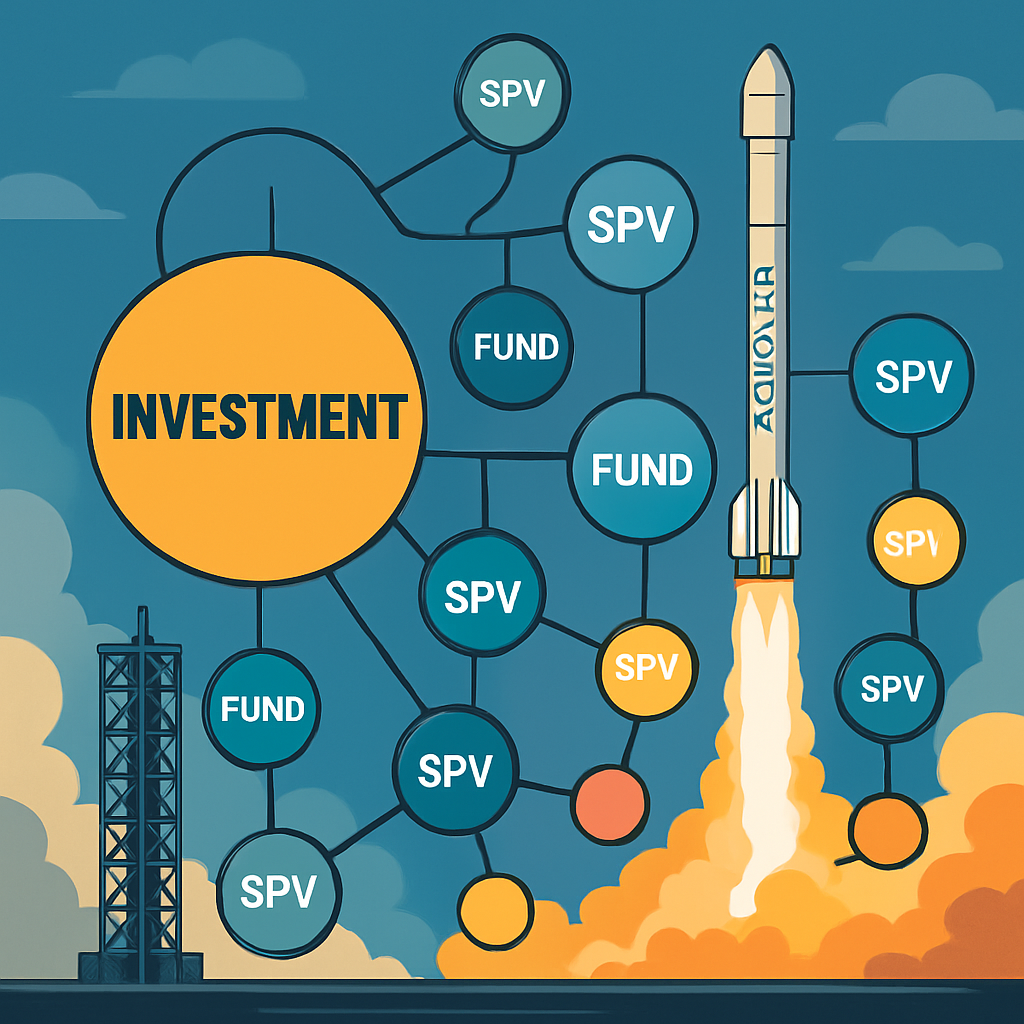

As SpaceX prepares for its public debut, investors who participated through special purpose vehicles (SPVs) are encountering significant uncertainties regarding their share entitlements. SPVs, which pool funds from multiple investors to invest in a single company, have been a common investment method. However, the complexity of multi-layered SPV structures in SpaceX’s case has introduced unprecedented challenges.

In recent years, the high demand for SpaceX shares led to the creation of SPVs nested within other SPVs, resulting in structures with multiple layers. This intricate arrangement means that investors in lower-tier SPVs may not know the exact number of shares they own or, in some cases, whether they will receive any shares at all.

The distribution of shares to SPV investors is further complicated by the company’s rolling lock-up periods, which are scheduled to lift over approximately four months. Lock-up agreements are standard practice to prevent insiders from selling shares immediately after an IPO, thereby avoiding excessive selling pressure on the stock. SPV managers typically cannot distribute shares to their investors until they themselves have access to the shares, leading to potential delays.

For instance, the first-layer SPV has 30 days to distribute stock to its investors. Consequently, subsequent layers may experience additional delays, with the bottom SPV layer potentially waiting eight to nine months for final disbursement. This staggered distribution timeline can result in investors receiving fewer shares than anticipated, as fees and administrative costs accumulate through each layer.

Communication challenges exacerbate the situation. Ideally, SPV managers should keep their investors informed from the IPO date onward. However, the multi-layered nature of these structures means that each participant may only be aware of information from the layer directly above them, leading to potential misunderstandings and misinformation.

There is also a risk that some investors may not receive any shares. Instances of fraudulent SPV managers fabricating access to non-existent allocations have occurred in the past, raising concerns about the legitimacy of some SPV sponsors. Investors at the bottom of these complex structures must trust that every manager above them is legitimate, a trust that may not always be warranted.

In light of these challenges, some companies, such as Anthropic and Anduril, have recently announced policies disallowing multi-layered SPV structures. This move aims to protect investors from the uncertainties and potential pitfalls associated with such complex arrangements.

The SpaceX IPO serves as a critical test case for the viability and transparency of multi-layered SPVs. Investors should exercise caution and conduct thorough due diligence when engaging in such investment vehicles, especially in high-demand scenarios where the temptation to create additional layers is strong. Clear communication and robust verification processes are essential to safeguard investor interests in these complex financial structures.