Cash App Introduces ‘Pay Later’ Feature for Peer-to-Peer Transfers

Cash App, the peer-to-peer financial technology platform owned by Jack Dorsey’s Block, has unveiled a new pay-over-time feature, enabling eligible users to defer payments for their everyday transfers. This development marks a significant expansion of flexible financing options into the realm of peer-to-peer (P2P) payments.

The Rise of Deferred Payment Options

In recent years, deferred payment services have gained traction across various sectors. For instance, approximately a year ago, DoorDash partnered with Klarna to allow users to finance their food orders, a move that sparked discussions about the implications of such financial practices. Cash App’s latest feature builds upon this trend, offering users the ability to manage their cash flow more effectively by spreading out payments over time.

How the ‘Pay Later’ Feature Works

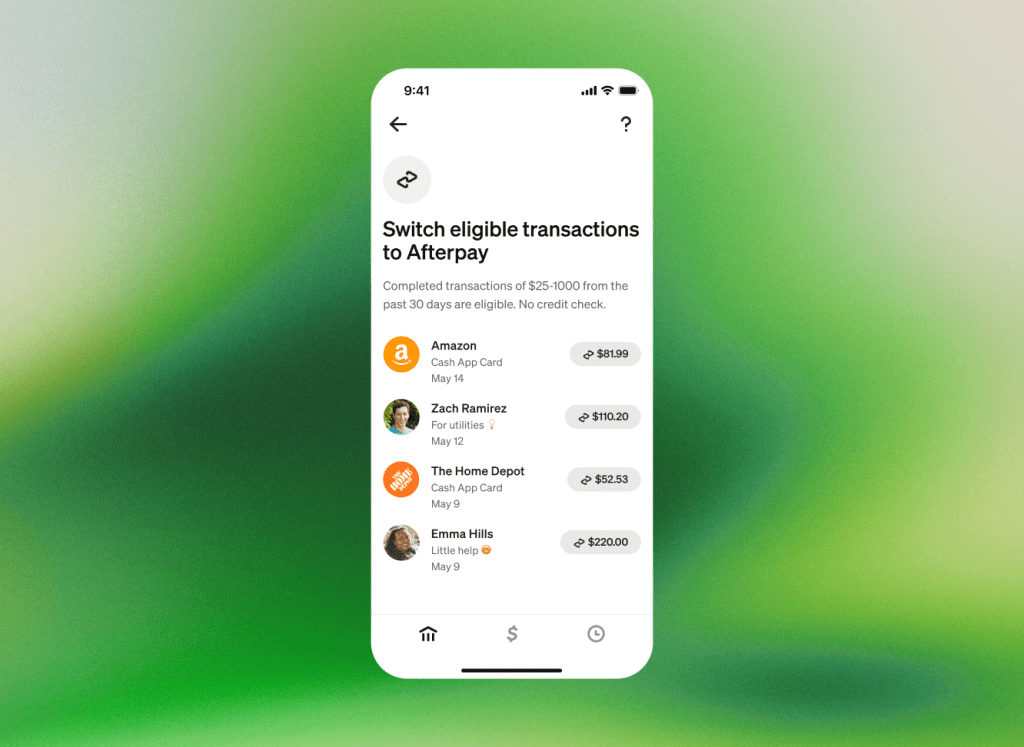

To utilize this new feature, users are required to pay a 7.5% fee. This means that borrowing $100 from Cash App would necessitate a repayment of $107.50. The service is available for transfers of $25 or more, with repayment options including weekly increments over a period of up to six weeks or a single payment at the due date.

Loan limits within this system are dynamic and tailored to individual users. A Cash App spokesperson explained, The specific amount available for conversion depends on the original transaction amount and individual customer assessment. We evaluate each transaction for eligibility based on our responsible lending criteria rather than setting traditional credit limits.

Addressing the Needs of a Changing Workforce

Owen Jennings, Block’s Executive Officer and Head of Business, highlighted that the new feature aims to provide value to Cash App’s customers through enhanced cash flow management. Jennings noted the evolving nature of the American workforce, with many individuals engaging in gig work, entrepreneurship, and multiple jobs, leading to variable income streams. He stated, We’re seeing more folks—particularly younger folks—who are solo-preneurs, entrepreneurs… [and] gig workers. They have side hustles, they’re working multiple jobs, [and] so they have variable income streams.

The Broader Context of ‘Buy Now, Pay Later’ Services

The popularity of buy now, pay later (BNPL) services has surged in recent years, offering consumers alternative financing options. However, these services have also faced criticism and legal challenges. Critics argue that such services can lead consumers into cycles of debt, and some view the need to finance basic household items as indicative of broader economic issues. Additionally, companies offering BNPL services have encountered legal scrutiny. For example, Klarna was recently sued in a class-action lawsuit alleging predatory practices.

Conclusion

Cash App’s introduction of the ‘pay later’ feature for P2P transfers reflects a growing trend in the financial technology sector to offer consumers more flexible payment options. While this feature provides users with additional tools for managing their finances, it also raises important questions about responsible lending practices and the potential implications for consumer debt. As the landscape of digital payments continues to evolve, both consumers and regulators will need to navigate these developments carefully.