Apple’s foray into the financial sector with the Apple Card Savings Account has garnered significant attention since its launch in April 2023. Partnering with Goldman Sachs, Apple introduced this high-yield savings account exclusively for Apple Card holders, offering an initial annual percentage yield (APY) of 4.15%. This move positioned Apple as a formidable contender in the competitive high-yield savings market.

Interest Rate Evolution

Over the past two years, the Apple Card Savings Account has experienced several interest rate adjustments, reflecting broader economic trends and decisions by the U.S. Federal Reserve. The APY peaked at 4.5% in early 2024 but has since been reduced in response to changing economic conditions. As of March 26, 2025, the APY stands at 3.75%, following a recent decrease from 3.9%. Despite this reduction, the Apple Card Savings Account remains competitive within the industry.

Comparative Analysis

When evaluating the Apple Card Savings Account against other high-yield savings options, it maintains a strong position. As of March 26, 2025, the APYs offered by various institutions are as follows:

– Ally Bank: 3.70% APY

– American Express: 3.70% APY

– Capital One: 3.70% APY

– Discover: 3.70% APY

– Marcus by Goldman Sachs: 3.75% APY

– Apple Card Savings: 3.75% APY

– SoFi Savings: 3.80% APY

– Wealthfront: 4.00% APY

– Robinhood: 4.00% APY

– Barclays Tiered Savings: 4.15%-4.40% APY

It’s noteworthy that traditional banking giants such as Chase, Bank of America, and Wells Fargo offer significantly lower interest rates, often below 0.03% APY. This stark contrast underscores the appeal of high-yield savings accounts like Apple’s for consumers seeking better returns on their deposits.

Features and Accessibility

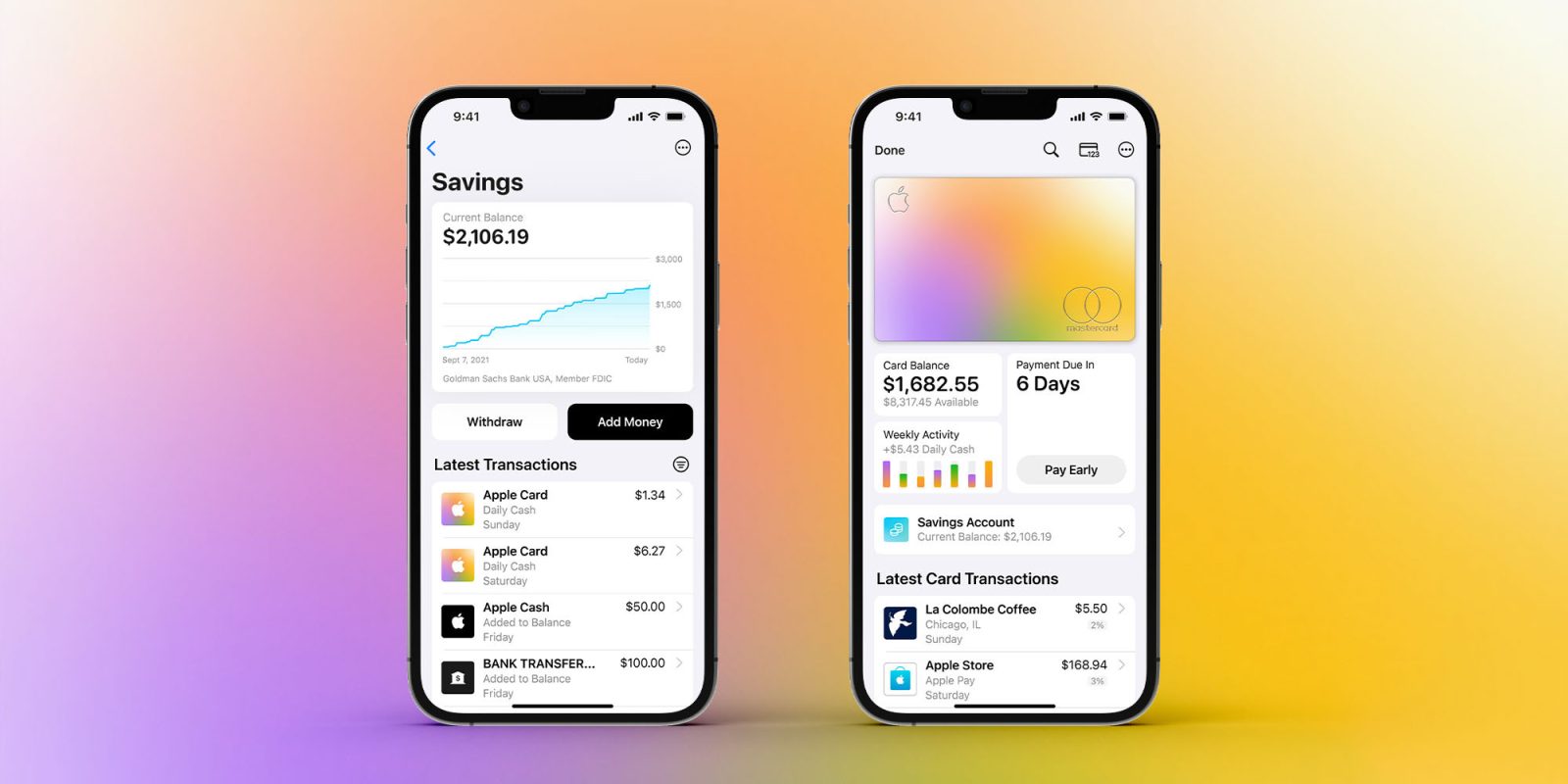

The Apple Card Savings Account is designed with user convenience in mind. Integrated seamlessly into the Wallet app on the iPhone, it allows Apple Card holders to:

– Automatic Daily Cash Deposits: Users can opt to have their Daily Cash rewards automatically deposited into their savings account, facilitating effortless savings growth.

– Additional Fund Deposits: Beyond Daily Cash, users can deposit funds from linked bank accounts or their Apple Cash balance, providing flexibility in managing their savings.

– No Fees or Minimums: The account boasts no fees, no minimum deposit requirements, and no minimum balance constraints, making it accessible to a broad range of users.

– High Balance Limit: The maximum balance allowed has been increased to $1 million, accommodating users with substantial savings.

Economic Context and Future Outlook

The fluctuations in the Apple Card Savings Account’s interest rate are reflective of broader economic dynamics, particularly the U.S. Federal Reserve’s monetary policies. As the Federal Reserve adjusts benchmark rates in response to economic indicators, financial institutions, including Apple and Goldman Sachs, correspondingly modify their offered APYs.

Looking ahead, the trajectory of the Apple Card Savings Account’s interest rate will likely continue to mirror these macroeconomic trends. For consumers, staying informed about such changes is crucial for making strategic financial decisions.

Conclusion

Despite recent reductions, the Apple Card Savings Account remains a competitive option in the high-yield savings market. Its integration with the Apple ecosystem, user-friendly features, and relatively high APY make it an attractive choice for Apple Card holders. As with all financial products, potential users should assess their individual needs and compare available options to determine the best fit for their financial goals.